The global market for Acoustic Doppler Current Profilers (ADCPs) — the essential instruments used to measure water current velocity across oceans, rivers, and coastal zones — reached $114 million in 2025 and is on track to hit $164 million by 2032, growing at a compound annual growth rate (CAGR) of 5.4%. Behind these headline figures, the real story is a market in structural transformation, with new applications and regions reshaping the demand landscape.

Growth Engine 1: Offshore Energy Becomes the Dominant Application

The biggest structural shift in ADCP demand is the rise of offshore energy. In 2024, the offshore-energy segment accounted for $330 million — 18% of the global ADCP market. By 2030, that share is projected to climb to 28%, overtaking traditional hydrology as the single largest application.

What’s driving this? Every utility-scale offshore wind farm requires 12–24 months of continuous current-profile data before construction even begins, plus operational-phase monitoring for foundation scour and cable burial assessment. With China alone targeting over 50 GW of offshore wind capacity by 2030, the ADCP procurement pipeline tied to renewable energy shows no sign of slowing.

Growth Engine 2: Asia-Pacific Emerges as the Growth Leader

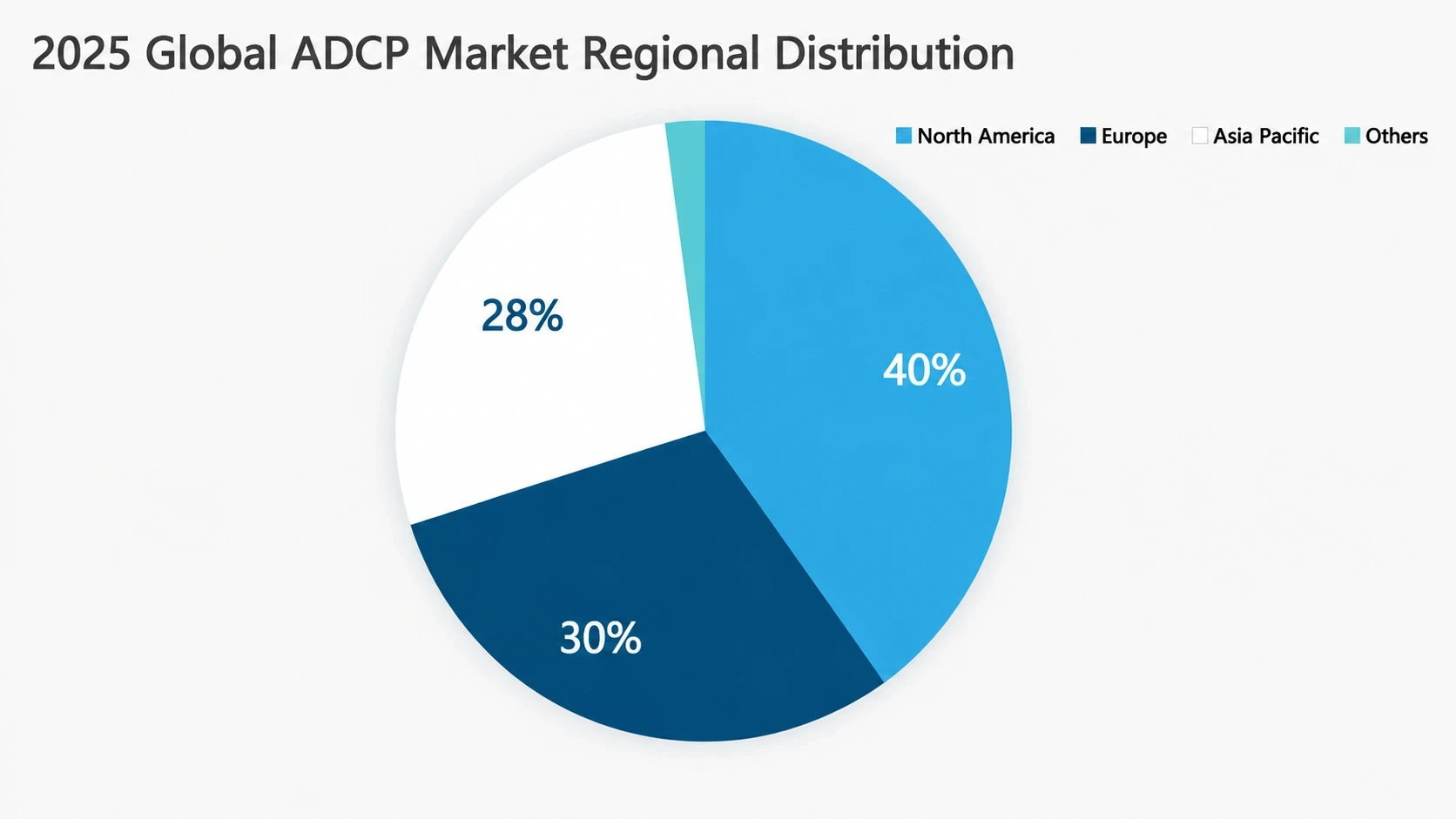

While North America still holds the largest regional share at ~40%, the Asia-Pacific region — led by China, Japan, and South Korea — is growing at more than double the global average. China’s ADCP market expanded 12.3% in 2025, fueled by three converging forces: the national “Maritime Power” strategy, the Smart Water Conservancy initiative, and aggressive domestic-technology substitution policies.

For global manufacturers, the message is clear: a presence in APAC is no longer optional. The region accounted for 28–33% of global revenue in 2025 and is gaining share every year.

Growth Engine 3: Technology Shifts Unlock New Use Cases

ADCPs are getting smaller, smarter, and more integrated. Instruments that once required a dedicated technician and a research vessel can now be deployed by a single person from a small boat — or left unattended on a buoy for months, transmitting data via satellite. Embedded AI processors perform real-time quality control and anomaly detection, transforming ADCPs from passive data loggers into intelligent observation nodes.

This technology evolution is expanding the addressable market: deep-sea aquaculture, urban flood-warning networks, submarine cable routing surveys, and coastal-resilience monitoring all represent new demand vectors that barely existed a decade ago.

The Bigger Picture

The ADCP market’s 5.4% CAGR tells only part of the story. Beneath that steady headline number, the market’s center of gravity is shifting — geographically toward Asia, sectorally toward offshore energy, and technologically toward AI-enabled integrated systems. Companies that align their product roadmaps and go-to-market strategies with these three vectors will capture disproportionate share of the $164M market that awaits in 2032.

For a complete analysis — including detailed regional breakdowns, profiles of all four leading manufacturers, and a five-year technology outlook — read the 2026 Global ADCP Industry White Paper.