An in-depth examination of the global Acoustic Doppler Current Profiler (ADCP) industry — from technological foundations to market forecasts, from incumbent leaders to emerging challengers, and from current drivers to the trends shaping the next five years.

Reading time: ~18 minutes | Published: June 9, 2026

Table of Contents

- Executive Summary: Why ADCP Matters

- What Is an ADCP? Core Technology & Value Proposition

- Industry Evolution: Four Decades of ADCP Development

- Global Market Landscape: Regional Analysis & Competitive Dynamics

- Profiles of Leading ADCP Manufacturers

- Growth Drivers: Policy, Demand, Technology & Competition

- 5-Year Outlook: ADCP Trends, 2026–2030

- Industry Challenges & Strategic Recommendations

- Key Takeaways

1. Executive Summary: Why ADCP Matters

The Acoustic Doppler Current Profiler (ADCP) is not merely another oceanographic instrument — it is the foundational tool for understanding how water moves across our planet. From the deep-ocean basins studied by climate scientists to the narrow irrigation channels monitored by water-resource agencies, ADCPs provide the velocity data that underpins critical decisions in energy, infrastructure, environmental protection, and national security.

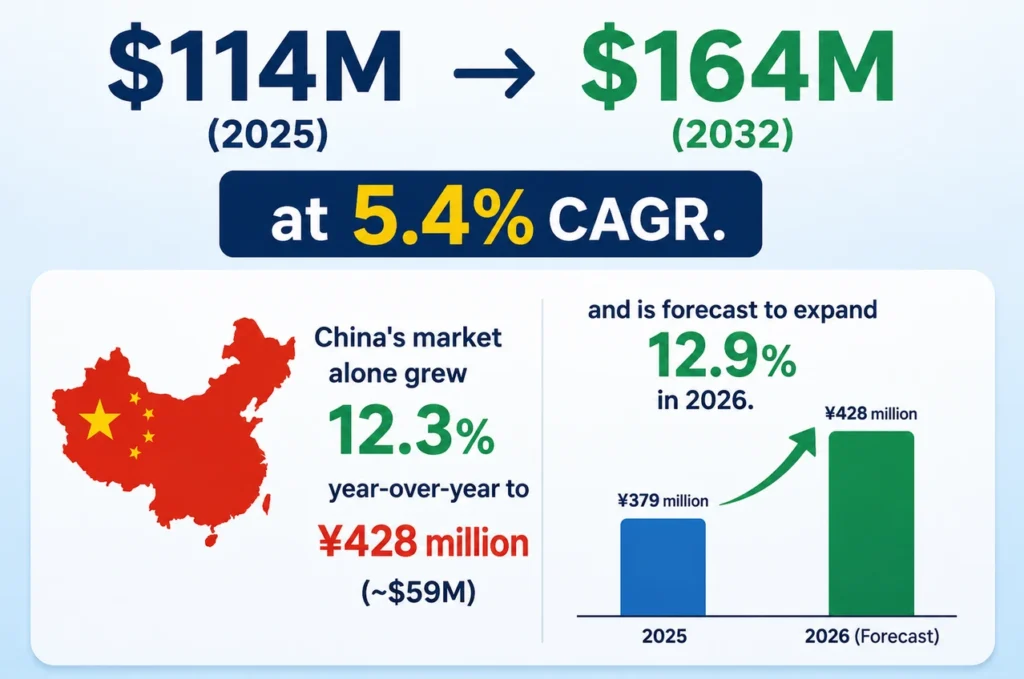

Key Market DataThe global ADCP market reached $114 million in 2025 and is projected to reach $164 million by 2032, growing at a CAGR of 5.4%. China’s market alone grew 12.3% year-over-year in 2025 to ¥428 million (~$59M), driven by offshore wind, smart water infrastructure, and domestic substitution policies.

This white paper provides a panoramic view of the global ADCP industry — tracing its technological evolution, mapping its geographical centers of gravity, profiling the companies that define its competitive landscape, and forecasting the forces that will reshape it through 2030. Whether you are an investor evaluating the hydrographic instrumentation space, an engineer specifying ADCPs for an offshore wind farm, or a policy maker shaping maritime strategy, this report offers the data and analysis you need.

2. What Is an ADCP? Core Technology & Value Proposition

2.1 How ADCP Technology Works

An Acoustic Doppler Current Profiler measures water velocity by exploiting the Doppler effect — the same physical principle that causes a passing ambulance siren to shift in pitch. An ADCP transmits short acoustic pulses into the water column through an array of transducers. As each pulse travels downward, suspended particles (sediment, plankton, bubbles) scatter a fraction of the acoustic energy back toward the instrument. By measuring the frequency shift of these returning echoes and knowing the speed of sound in water and the beam geometry, the ADCP calculates the three-dimensional velocity of the water at discrete depth bins — typically from a few centimeters to tens of meters thick — across the entire profile.

A modern ADCP integrates four core subsystems:

- Transducer Array: Typically 3–9 piezoelectric ceramic elements that transmit and receive acoustic signals. Beam configurations range from the classic 4-beam Janus arrangement to advanced 9-beam phased arrays.

- Signal Processing Unit: Onboard DSP and increasingly embedded AI processors that convert raw acoustic returns into calibrated velocity estimates in real time.

- Auxiliary Sensors: GPS/GNSS for positioning, attitude and heading reference systems (AHRS) for motion compensation, pressure sensors for depth, and optionally CTD (conductivity-temperature-depth) for sound-speed correction.

- Power & Storage: Battery systems optimized for autonomous deployments ranging from hours to years, coupled with solid-state storage or real-time telemetry.

ADCPs are categorized by deployment mode: vessel-mounted (survey boats, ships of opportunity), moored/bottom-mounted (long-term fixed stations), lowered (CTD-rosette profiling), and autonomous (integrated on AUVs, gliders, or buoys). Operating frequencies span 38 kHz (deep-ocean, ranges exceeding 1,000 m) to 3,000 kHz (laboratory-scale turbulence studies), with the 75–1,200 kHz band covering most field applications. Explore Oceantek’s full range of ADCP products for specific deployment scenarios.

2.2 Why ADCP Outperforms Legacy Current Measurement

Compared with traditional single-point current meters (rotor-type, electromagnetic, or acoustic point sensors), ADCPs offer three transformative advantages:

- Full-Profile Coverage: A single ADCP replaces an entire mooring string of point current meters, delivering continuous velocity profiles from near-surface to near-bottom — a three-dimensional picture of the flow field in one deployment.

- Non-Intrusive, Fast Measurement: ADCPs measure remotely (the sampling volume is typically 0.5–5 m from the transducer face), eliminating flow disturbance. A profile can be acquired in seconds to minutes, versus the hours required to lower and recover a mechanical current meter at multiple depths.

- Multi-Environment Adaptability: The same instrument platform can be configured for shallow rivers (< 1 m depth), continental-shelf waters, or full-ocean-depth deployments (6,000 m rated). This versatility has been a key enabler of ADCP adoption across disciplines.

| Domain | Key Application | ADCP Value |

|---|---|---|

| Oceanography | Boundary current monitoring, water-mass transport | Long-range profiling captures full-depth transport estimates |

| Offshore Energy | Wind-farm site assessment, turbine foundation scour | Continuous current profiles for engineering design & monitoring |

| Hydrology | River discharge measurement, flood forecasting | Rapid, repeatable discharge measurements without wading or cableways |

| Ports & Coastal Engineering | Dredging monitoring, siltation studies | Real-time suspended-sediment flux estimates |

| Climate Research | Meridional overturning circulation, heat flux | Multi-year moored ADCP arrays for decadal climate signals |

| Defense | Underwater navigation, amphibious operations | Tactical current nowcasts for dive and landing planning |

| Aquaculture | Deep-sea cage siting, waste dispersion | High-resolution current mapping for environmental compliance |

| Inland Waterways | Irrigation canal monitoring, ecological baseflow | Low-cost, side-looking ADCP for permanent installations |

Table 1: ADCP Application Domains & Value Delivered

3. Industry Evolution: Four Decades of ADCP Development

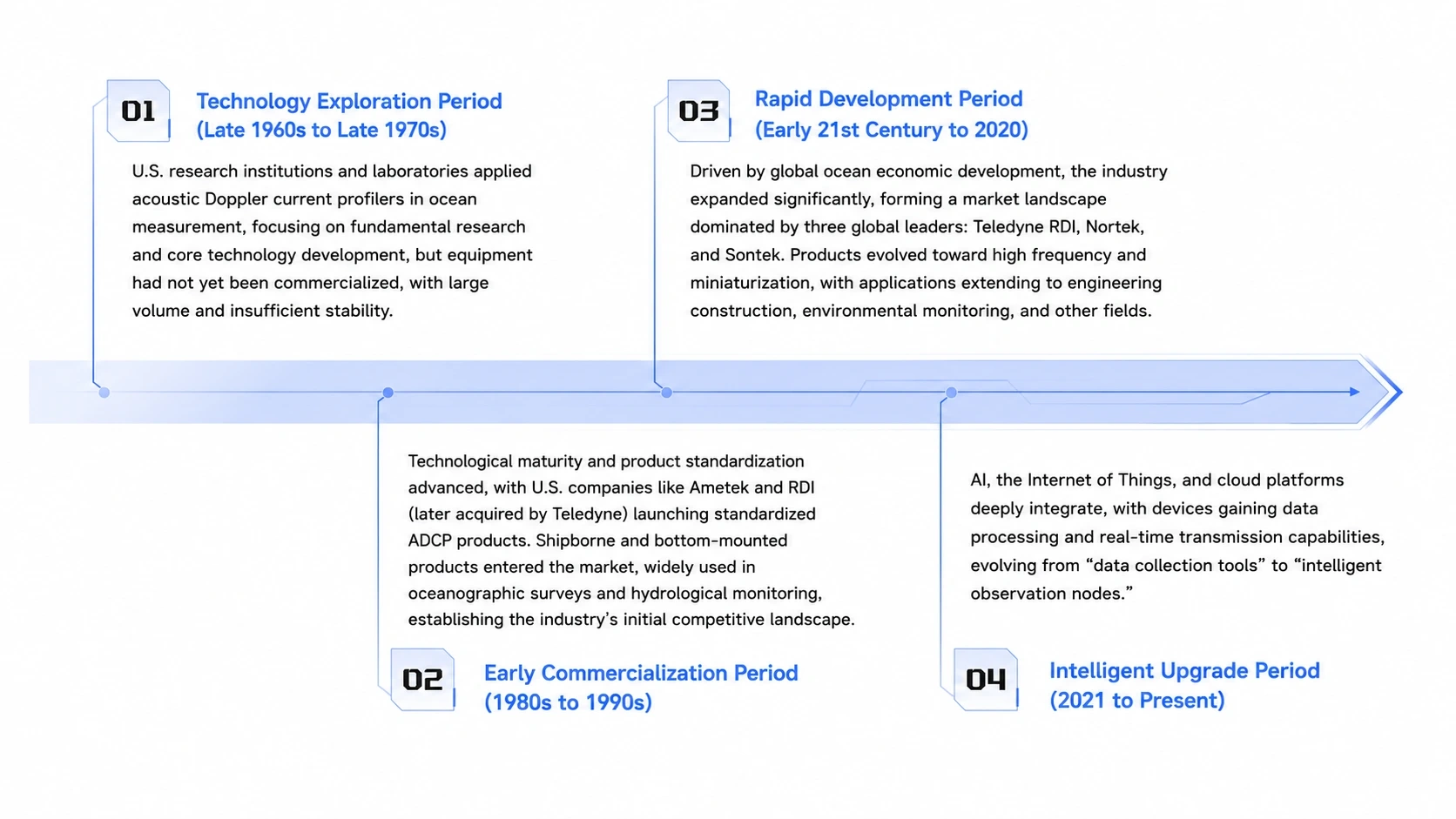

The ADCP industry traces a path from laboratory curiosity to AI-enabled intelligent sensor — a journey driven by the co-evolution of acoustics, electronics, and the expanding ambitions of ocean science and marine engineering. This evolution can be divided into four distinct phases.

Phase 1: Laboratory Exploration (1960s–Late 1970s)

The foundational decade. Research groups in the United States — notably at the Woods Hole Oceanographic Institution, Scripps Institution of Oceanography, and the NOAA Environmental Research Laboratories — conducted the first proof-of-concept experiments demonstrating that the Doppler shift of acoustic backscatter could reliably measure water velocity at range. These early systems were rack-mounted, power-hungry, and confined to research vessels. They proved the physics worked; commercialization was still a distant prospect.

Phase 2: Commercial Emergence (1980s–1990s)

This period saw the transition from bespoke lab instruments to field-ready commercial products. Ametek and RD Instruments (RDI) in the United States led the charge, releasing the first standardized vessel-mounted and moored ADCPs. The 150 kHz Workhorse ADCP (RDI, early 1990s) became an industry workhorse — reliable, repeatable, and deployable by a single technician. By the mid-1990s, Teledyne had acquired RDI, forming Teledyne RDI and setting the stage for industry consolidation. Nortek (Norway) entered the market in the late 1990s with a focus on compact, user-friendly instruments for coastal applications, while Sontek (USA, later acquired by YSI/Xylem) carved out a niche in shallow-water hydrology.

Phase 3: Rapid Expansion (2000–2020)

The new millennium brought a surge in ocean observation infrastructure. The Global Ocean Observing System (GOOS), the Argo float program, and the Ocean Observatories Initiative (OOI) created sustained demand for current-profiling instruments. The ADCP product category diversified: phased-array ADCPs achieved deep-ocean profiling ranges, while high-frequency (600–1,200 kHz) instruments enabled turbulence-resolving measurements in shallow water. Multi-sensor integration emerged — combining ADCPs with CTDs, turbidity sensors, and optical plankton counters. By 2020, three firms — Teledyne RDI, Nortek, and Sontek — controlled the majority of the global market. A fourth player, Oceantek (China), began gaining traction with competitively priced instruments tailored to the demanding conditions of Asian marginal seas.

Phase 4: Intelligent Integration (2021–Present)

The current era is defined by the convergence of ADCP hardware with artificial intelligence, IoT connectivity, and cloud computing. Modern ADCPs are no longer passive data loggers — they are intelligent observation nodes that process data on-board, transmit results in near-real time via satellite or cellular networks, and adapt their sampling strategies to changing environmental conditions. The competitive frontier has shifted from hardware specifications alone to the quality of integrated hardware + data services. Applications are pushing into ultra-deep water (>6,000 m), the polar regions, and autonomous platforms that operate without human intervention for months at a time.

Figure 1: The Four Phases of Global ADCP Industry Evolution

4. Global Market Landscape: Regional Analysis & Competitive Dynamics

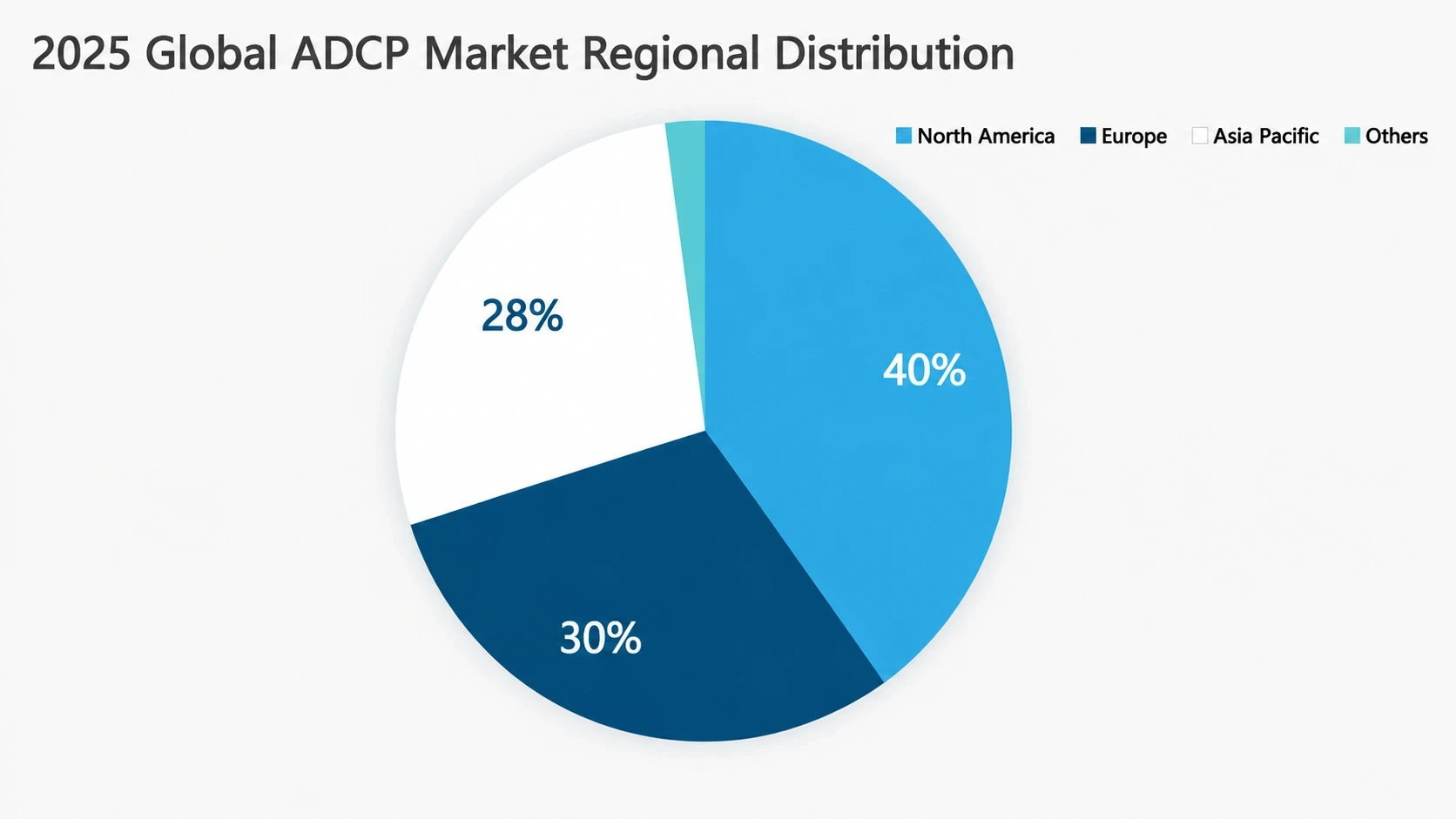

The global ADCP market is structured around three core regions — North America, Europe, and Asia-Pacific — each with a distinct profile in terms of technological capability, demand drivers, and market maturity.

4.1 North America: Technology Leader & Market Anchor

- Share: ~40% of the global market (2025 estimate).

- Strengths: The United States maintains a complete RD&E–manufacturing–applications ecosystem. Decades of sustained federal investment through NOAA, NSF, ONR, and USGS have built an unmatched installed base and technical workforce.

- Demand Drivers: Deep-ocean research, naval applications, offshore oil & gas decommissioning and re-purposing for carbon storage, and the expanding U.S. offshore wind pipeline (30 GW target by 2030).

- Key Applications: Basin-scale ocean observing, defense hydrography, offshore energy site characterization, and large-river discharge monitoring (Mississippi, Columbia).

4.2 Europe: Specialized Excellence & Steady Growth

- Share: 25%–30% of the global market.

- Strengths: Norway, the UK, and Germany lead in specialized segments — high-frequency turbulence profilers, polar-rated instruments, compact integrated systems for coastal engineering. EU framework programs (Horizon Europe) and national research councils provide sustained R&D funding.

- Demand Drivers: Offshore wind (Europe has >30 GW installed), marine environmental monitoring under the Marine Strategy Framework Directive, Arctic research, and port infrastructure modernization.

- Key Applications: Wind-farm foundation scour monitoring, tidal-stream energy resource assessment, fjord circulation studies, and harbour siltation management.

4.3 Asia-Pacific: The High-Growth Frontier

- Share: 28%–33% and rising fast.

- Strengths: China is the region’s growth engine, driven by aggressive national policies for maritime sovereignty (“Maritime Power” strategy), smart water infrastructure, and domestic technology substitution. Japan and South Korea contribute significant demand from their shipbuilding and ocean-engineering sectors.

- Demand Drivers: China’s offshore wind build-out (the world’s largest by installed capacity), the South-to-North Water Diversion Project and associated hydrological monitoring, “Sponge City” flood-management programs, and the rapid expansion of deep-sea aquaculture.

- Key Applications: River-discharge measurement networks, near-shore construction monitoring, maritime-silk-road port development, and AUV/ROV-based marine surveying.

Figure 2: Global ADCP Market — Regional Revenue Share (2025 Estimate)

| Region | Market Share (2025E) | Growth Rate | Primary Sectors |

|---|---|---|---|

| North America | ~40% | Moderate (~4%) | Deep-sea research, defense, offshore energy |

| Europe | 25–30% | Steady (~5%) | Offshore wind, polar research, coastal engineering |

| Asia-Pacific | 28–33% | High (>10%) | Hydrology, offshore wind, smart water, aquaculture |

| Rest of World | ~5% | Variable | Port development, resource exploration |

Table 2: Regional Market Summary

5. Profiles of Leading ADCP Manufacturers

Four companies define the competitive landscape of the global ADCP industry. Each occupies a distinct strategic position defined by technology portfolio, target markets, and geographic strength.

5.1 Teledyne Marine (USA) — The Industry Benchmark

Positioning: The undisputed technology leader and market-share leader in the global ADCP industry. Teledyne RDI (the ADCP business unit within Teledyne Marine) serves the most demanding customers in ocean science, naval operations, and offshore energy. Its instruments set the de facto standard against which competitors are measured.

Technology Highlights

- Broadband & Phased-Array Processing: Proprietary signal-processing techniques that dramatically improve precision for a given averaging interval — a defining competitive advantage in deep-water and low-scattering environments.

- 4-Beam Redundancy: The Janus configuration with an additional vertical beam (4-beam + vertical) provides error-velocity estimates and surface-track capability.

- Frequency Range: 38 kHz (deep-ocean) to 1,200 kHz (shallow/high-resolution). Depth rating to 6,000 m.

- Recent Innovation: Embedded AI processing for adaptive sampling, real-time quality control, and edge-computing applications.

Core Markets: Global ocean observing systems, academic fleet operations, defense hydrography, deep-water oil & gas, and offshore wind resource assessment.

5.2 Nortek (Norway) — The Coastal & Engineering Specialist

Positioning: Nortek has built its reputation on ease of use, multi-parameter integration, and robustness in challenging coastal environments. Headquartered outside Oslo, the company punches above its weight in the European offshore-wind market and has a loyal following in the research community for its intuitive software ecosystem.

Technology Highlights

- Signature Series: The flagship product line integrating current profiling with wave-directional spectra, turbidity, and ice-thickness measurement in a single instrument.

- Concave Transducer Design: Flush-mount capability for hull installations on survey vessels and autonomous surface vehicles — reducing drag and biofouling vulnerability.

- Frequency Range: 55 kHz to 1,000 kHz. Mid-water (continental-shelf) deployments are a particular strength.

- Software: Unified acquisition and post-processing environment, with cloud-based data management for fleet deployments.

Core Markets: Offshore wind foundation monitoring, tidal-energy site characterization, estuarine and delta sediment-transport studies, and Arctic/Antarctic research.

5.3 Sontek (USA, Xylem/YSI) — The Hydrology & Shallow-Water Authority

Positioning: Sontek dominates the market for shallow-water, riverine, and engineered-channel applications. As part of Xylem’s YSI water-quality division, Sontek benefits from a global distribution network and brand recognition in the water-resources sector that competitors cannot easily replicate.

Technology Highlights

- M9 Series (Flagship): A 9-beam, multi-frequency system that automatically adapts its acoustic parameters to water depth and turbidity, delivering high-quality discharge measurements without expert tuning.

- SL Series (Side-Looking): Designed for permanent installation on bridge piers, canal walls, and culvert sides — a form factor unique to Sontek’s hydrology market.

- Pulse-Coherent Mode: Enables millimeter-per-second velocity resolution in water depths as shallow as 10 cm.

Core Markets: USGS-style discharge measurement, urban flood-warning networks, irrigation-district water accounting, and ecological baseflow assessment.

5.4 Oceantek (China) — The Emerging Challenger

Positioning: Oceantek has rapidly established itself as China’s leading domestic ADCP brand and an increasingly credible competitor in international markets. The company’s strategy centers on algorithmic differentiation for complex-water environments — specifically high-sediment, high-turbidity, and strong-tidal conditions common in Chinese and Southeast Asian waters — combined with aggressive weight and cost reduction enabled by in-house transducer design.

Technology Highlights

- Full Product Portfolio: 75 kHz, 300 kHz, 600 kHz, M9, and river-type HADCP covering all deployment scenarios from deep-sea to wadeable streams.

- Titanium-Alloy Housing (Standard): All non-HADCP models ship with titanium housings rated to 6,000 m, a premium feature that is typically a costly upgrade from competitors.

- Proprietary Sediment-Tolerant Algorithms: Purpose-built signal processing for high-turbidity (>10 g/L suspended sediment) and macro-tidal (>5 m range) environments — conditions where standard ADCP algorithms can lose bottom-track or produce biased velocities.

- Weight Advantage: The 600 kHz model weighs 3.5 kg (~30% lighter than comparable imports); the river-type M9 weighs ≤1.5 kg, enabling single-person deployment.

- Accuracy: ±0.3% of measured velocity ±3 mm/s, validated in third-party intercomparison studies.

Core Markets: Maritime Silk Road port and waterway surveys, China’s national hydrological network, offshore wind-farm construction monitoring (particularly in the South China Sea and East China Sea), AUV/ROV payload integration, and long-duration subsurface mooring observations.

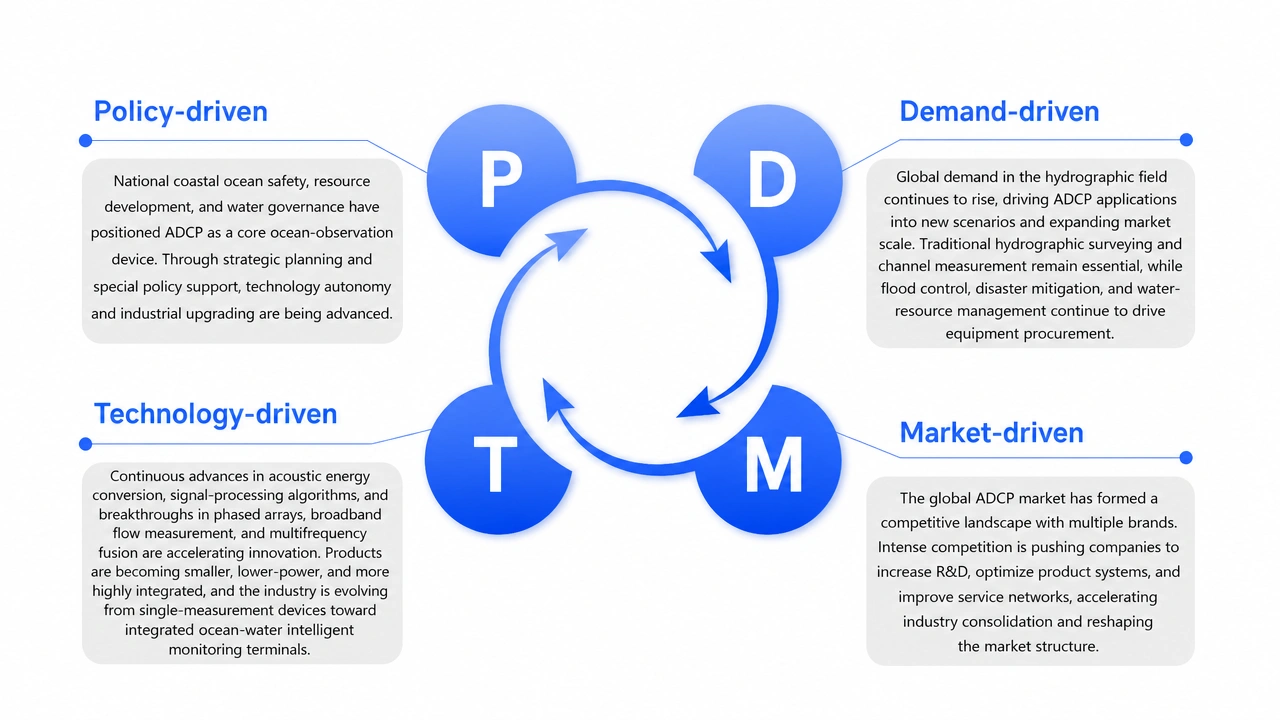

6. Growth Drivers: Policy, Demand, Technology & Competition

The ADCP industry is propelled by four interlocking drivers. Policy creates the mandate; demand generates the revenue; technology enables new capabilities; and competition accelerates the innovation cycle.

6.1 Policy: National Strategies Elevate ADCP to Critical Infrastructure

Governments around the world have classified ocean observation as a strategic priority, and ADCPs as essential infrastructure within that category:

- United States: The National Oceanographic Partnership Program (NOPP) and the NOAA Uncrewed Systems Strategy explicitly identify current-profiling as a core capability. The FY2025 federal ocean-observation budget exceeded $1.2 billion, with ADCP procurement embedded in fleet modernization and observing-system maintenance.

- Norway: The government’s “Blue Ocean” strategy and NATO’s Science for Peace and Security program continue to fund Nortek-relevant R&D, particularly for Arctic monitoring and offshore renewable energy.

- China: The “Maritime Power” (海洋强国) national strategy and the “Smart Water Conservancy” (智慧水利) initiative set explicit targets for domestic ADCP production and deployment. Government procurement policies increasingly favor domestically manufactured instruments, accelerating the growth of firms like Oceantek.

6.2 Demand: Expanding Applications Drive Market Growth

Demand-side expansion is the most powerful near-term catalyst. Traditional hydrological monitoring and nautical charting remain the bedrock — accounting for roughly 48% of unit sales — but the growth is coming from emerging sectors:

- Offshore Wind: Each utility-scale wind farm requires extensive pre-construction current profiling (12–24 months of moored ADCP data) plus operational-phase monitoring. China’s offshore-wind-related ADCP demand grew >15% year-over-year in 2024–2025.

- Deep-Sea Aquaculture: The global expansion of offshore fish farming — particularly in Norway, Chile, and China — requires continuous current monitoring for cage-structure integrity, feed dispersion, and environmental compliance.

- Submarine Cable & Pipeline Routing: The global submarine-cable market (driven by data-center interconnection and offshore wind export cables) requires detailed current surveys for burial-depth assessment and scour prediction.

- Coastal Resilience: Sea-level rise and storm-surge modeling increasingly depend on long-duration ADCP datasets for model calibration and validation.

Growth SpotlightThe offshore-energy ADCP segment reached $330 million in 2024 (18% of the global total) and is projected to rise to 28% by 2030, making it the single largest application segment within the forecast period.

6.3 Technology: Smarter, Smaller, More Integrated

Three technology vectors are reshaping what ADCPs can do:

- AI & Edge Computing: Embedded machine-learning models now perform real-time data-quality assessment, biofouling detection, and adaptive sampling-rate adjustment — functions that previously required post-cruise processing by a trained analyst.

- Miniaturization & Low Power: Advances in transducer materials (piezoelectric composites, MEMS) and low-power electronics have produced ADCPs weighing under 3.5 kg — a trend exemplified by Oceantek’s lightweight ADCP lineup with power draws measured in milliwatts — enabling deployment on small autonomous vehicles and solar-powered fixed stations.

- Multi-Sensor Fusion: The latest instruments natively integrate current profiling with CTD, turbidity, dissolved oxygen, chlorophyll fluorescence, and passive-acoustic monitoring — transforming the ADCP from a single-purpose current meter into a compact ocean-observing hub.

6.4 Market Competition: A Race on Precision, Price & Platforms

The global ADCP market is shifting from a comfortable oligopoly to a more contested landscape. Incumbents (Teledyne, Nortek, Sontek) are defending their positions by deepening their moats in high-end scientific and defense markets, while emerging players (led by China’s Oceantek) are leveraging cost competitiveness, faster customization cycles, and growing in-market references to win tenders in price-sensitive segments. Competition is increasingly multidimensional — accuracy × environmental robustness × software ecosystem × total cost of ownership — which benefits end users but puts pressure on margins across the industry.

Figure 3: The Four-Pillar Framework of ADCP Industry Growth

7. 5-Year Outlook: ADCP Trends, 2026–2030

7.1 Market Size & Growth Forecast

| Metric | 2025 (Actual) | 2026E | 2032E | CAGR |

|---|---|---|---|---|

| Global Market (USD) | $114M | ~$120M | $164M | 5.4% |

| China Market (CNY) | ¥428M | ¥481M | — | ~12.9% (near-term) |

| Offshore Energy Share | 18% | ~20% | ~28% | Expanding |

| Traditional Hydrology Share | 48% | ~45% | ~38% | Contracting |

7.2 Four Trends Defining the Next Five Years

Trend 1: Deep AI Integration — From “Data Collector” to “Decision Engine”

By 2030, expect ADCPs that do more than measure and report. Embedded AI models — trained on decades of oceanographic data — will perform in-situ trend detection, anomaly alerting, and predictive current forecasting. An ADCP deployed on an offshore platform will not just log the current profile; it will autonomously detect an approaching eddy, predict its impact on operations, and alert the platform control room — without a human in the loop.

Trend 2: Multi-Function Integration — One Platform, Many Parameters

The ADCP is becoming the central nervous system of a multi-parameter observing platform. Future instruments will natively fuse current, wave, water-quality, bioacoustic, and meteorological data streams, communicating via standardized protocols (Sensor Web Enablement, OGC APIs) into integrated ocean-digital-twin environments. This trend is already visible in Nortek’s Signature and Teledyne’s Workhorse II platforms.

Trend 3: Pervasive Sensing — Miniaturized, Mesh-Networked, Everywhere

MEMS-based acoustic transducers and ultra-low-power system-on-chip designs are driving ADCPs toward the size, cost, and power envelope of a consumer-electronics device. This opens the door to large-scale mesh deployments — tens or hundreds of ADCPs distributed across a bay, estuary, or reservoir, communicating via underwater acoustic networks or pop-up satellite telemetry. “Pervasive ocean sensing” — long a slogan — is approaching technical feasibility.

Trend 4: Data-as-a-Service — Monetizing the Data Stream

The industry’s business-model center of gravity is shifting from selling boxes to selling data subscriptions and analytics services. Customers increasingly want guaranteed data availability (99% uptime SLAs), cloud-based visualization dashboards, and API access to quality-controlled data streams — not just a calibrated instrument in a crate. This “hardware + SaaS” model increases customer stickiness and recurring revenue, and is becoming a key competitive differentiator.

8. Industry Challenges & Strategic Recommendations

8.1 Core Challenges

- Technology Barriers Remain High: Critical components — particularly broadband transducers, high-efficiency power amplifiers, and radiation-hardened electronics for space-constrained platforms — still depend on a limited number of specialized suppliers. R&D cycles are long (3–5 years for a new platform) and capital-intensive, creating a significant barrier to new entrants.

- Raw-Material Cost Volatility: Piezoelectric ceramics (PZT), titanium alloys, and specialty polymers — all essential ADCP materials — are subject to global commodity cycles and trade-policy disruptions. The 2024–2025 spike in rare-earth magnet prices, for example, directly compressed margins across the hydroacoustic-instrument supply chain.

- Talent Scarcity: ADCP development requires a rare combination of skills — underwater acoustics, embedded systems, signal processing, oceanography, and mechanical design for pressure-tolerant structures. The global pool of experienced ADCP engineers is measured in hundreds, not thousands.

8.2 Strategic Recommendations

- Invest in University–Industry Consortia: The most successful firms in this industry (Teledyne RDI, Nortek) have deep, multi-decade relationships with oceanographic research institutions. Emerging players should formalize R&D partnerships with university acoustics labs and ocean-engineering departments to accelerate technology development and build their talent pipelines.

- Diversify & Regionalize Supply Chains: Reducing single-source dependency — particularly for transducers and titanium fabrications — should be a board-level priority. Regionalizing supply chains (Americas, EMEA, APAC) adds resilience against trade disruptions and can reduce logistics costs.

- Build Talent with Competitive Incentives: Firms should establish fellowship programs, sponsor PhD research, and offer equity-based compensation to attract and retain the multidisciplinary engineers who design the next generation of ADCPs. The industry competes for talent not just internally, but with the broader sensor, autonomous-vehicle, and defense-electronics sectors.

- Embrace the Data-Services Transition: Hardware margins will continue to compress as competition intensifies. The long-term value lies in building platforms that generate recurring data-service revenue — analytics, monitoring-as-a-service, and integrated decision-support tools for maritime operators.

9. Key Takeaways

- The global ADCP market is a $114M industry growing at 5.4% CAGR, projected to reach $164M by 2032.

- Three regions dominate — North America (~40%), Europe (25–30%), and Asia-Pacific (28–33%) — with APAC growing fastest, driven by China’s maritime infrastructure build-out.

- Four manufacturers define the competitive landscape: Teledyne RDI (deep-ocean leader), Nortek (coastal engineering specialist), Sontek (hydrology authority), and Oceantek (emerging challenger with cost and complex-water advantages).

- Offshore energy is the single largest growth vector. Offshore-wind-related ADCP demand is growing >15% annually in China, and the segment is projected to reach 28% of the global market by 2030.

- The technology frontier is shifting from hardware specifications to AI-enabled edge computing, multi-sensor integration, miniaturization, and data-as-a-service business models.

- Competition is intensifying. Incumbents are defending high-end markets, while emerging players leverage cost advantages and faster customization — a dynamic that will accelerate innovation but compress margins.

- Strategic success over the next five years will depend on deepening university partnerships, diversifying supply chains, winning the talent war, and transitioning to recurring data-service revenue.

Disclaimer: This white paper is based on publicly available data and industry experience. All market figures, forecasts, and company assessments are provided for informational purposes only and do not constitute investment advice. Market conditions and technology developments are subject to change; readers are encouraged to consult the latest industry sources.